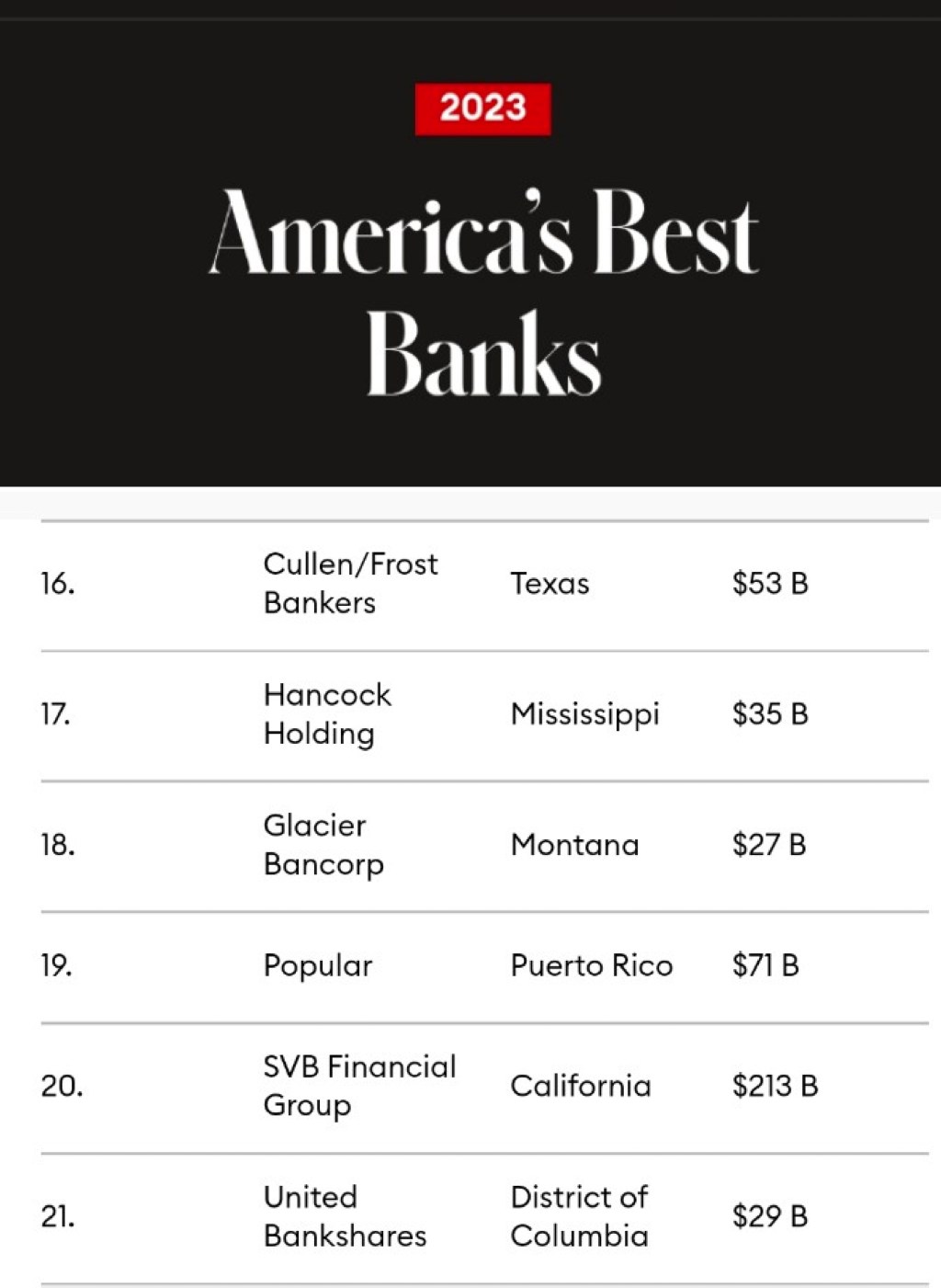

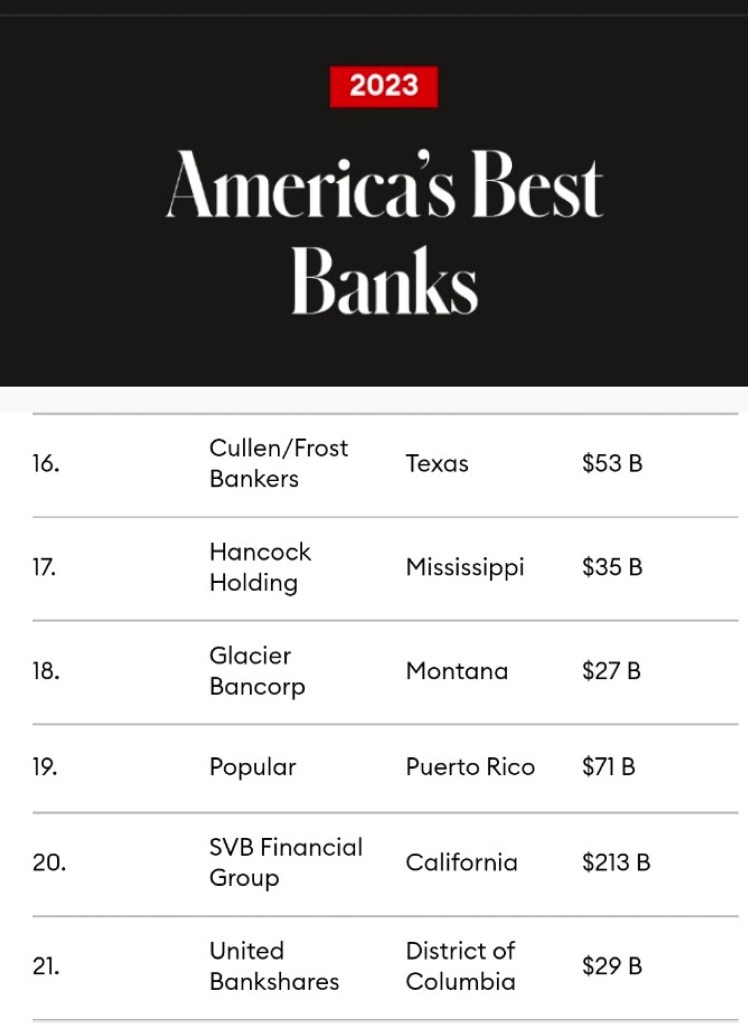

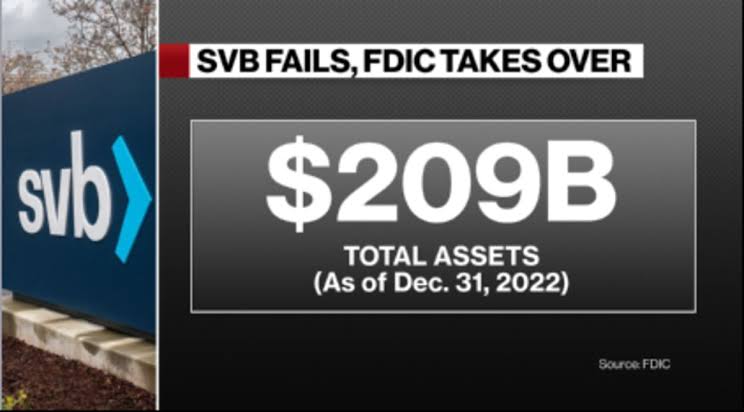

This is forbes magazine on the 14th of february 2023 the title of this particular article reads america’s best banks an entity by the name of silicon valley bank was ranked number 20th and has been on the list for five years in a row founded in 1983 svb was the 16th largest bank in the united states and had over 209 billion dollars in assets yet in a few short weeks the bank would go up in flames over the course of a couple of days.

The crash created a cascade of events: some smaller regional banks lost the majority of evaluation and another has since collapsed.

Companies such as Roblox, vox media and a whole lots of silicon valley startups are scrambling to find the cash to pay their employees, meanwhile the UK government is at work trying to minimize the effects of the crash and at the same time the rest of the economy is trying to figure out what the long term consequences of this disaster maybe this is the largest bank failure since 2008 and the 2nd largest in history.

But how did a bank go from making the list of the best banks to bankruptcy in less than a month? What happens next? Is this the start of another financial crisis? Maybe not but there are some risks. What everyone seems to have missed in the story is that it’s more of a cautionary tale of mismanagement incompetent and political lobbying. The bank’s parent company, its CEO and CFO are all being sued for fraud and the CEO lobbied congress to remove the very laws that would have prevented this crash in the first place. This whole thing is a crazy story so let’s get into it.

To understand the consequences of this crash we need to know how it started. Silicon valley bank or SVB was no ordinary bank, it was the go-to institution for venture capital and tech startups. The bank enjoyed a healthy period of growth during the 2020 pandemic; low interest rates and excessive money printing from the US federal reserve caused the tech sector to boom.

Money was easy and investors were generous. At the time startups were able to raise money easily due to cheap credit. Once the company’s got that money they needed somewhere to store it, this is where silicon valley bank comes in. SVB was very popular among founders in fact nearly 50% of all United States Start-ups have some deposits in silicon valley bank.

And in 2021 svb saw a massive influx and deposits. From around $61 billion at the end of 2019 to around $189 billion at the end of 2021.

Now svb wanted to make a larger profit from all of this cash that they were suddenly sitting on.

A safe investment would be long term bonds, these are usually seen as safer than stocks and provide a steady return. Here is why, when interest rates are low newly issued bonds pay lower interest rates or returns making existing long term bonds that pay higher more attractive this leads to an increase in demand for these bonds and an increased in their price so whoever is holding these long term bonds makes money.

SVB saw this situation and invested $80 billion dollars of their tech company deposits in long term bonds and other securities. They could then turn around and pay depositors a lower rate. The difference between the high rates from their long term bonds and the cost of lower rates for their deposits would be their profit. This arrangement works particularly well even if some clients decide to withdraw sooner the bank can simply sell the bond and get the liquidity necessary to pay back the depositor.

But what happens when everyone wants to withdraw their money all at once?

Silicon valley bank was about to find out.

After the 2008 financial crisis, the post crisis market isn’t used to a high interest rate environment and higher interest rates could create risks in vulnerable areas of the financial system. The risk management team of svb ignored this risk but more on this later.

Problems for svb began brewing in late 2021 in the United states inflation began to rise. Usually when this happens the us federal reserve would increase interest rates to slow the economy and counteract the inflation but this time the us federal reserve stood by and did nothing for a while they told everyone that inflation was transitory.

This turned out to be completely wrong and when the fed realize their mistake the had to raise interest rates very quickly to make up for lost time, this whiplash and higher rates didn’t allow time for the market to adjust. Meanwhile at svb their investing environment began to flip on his head as the interest rates rose the newly issued bonds began to pay high interest rates and this might make the older long term bond less attractive to investors. This resulted in a decline in demand causing their prices to fall. SVB still owned tens of billions worth of these long term bonds so they were sitting duck for risk.

By the end of 2022 there were $15 billion dollars in unrealized losses from the fall in long term prices.

Now normally this isn’t an issue as if svb held onto these bonds until maturity they wouldn’t lose anything but this was not a normal time.

In a high interest rate environment technology startups was struggling to get financing as credit began to dry up these tech companies needed to dip into their cash to fund their operations.

With Start-ups being the main client for svb the deposit started to slow down. Falling from $189 billion at the end of 2021 to $173 billion at the end of 2022. With every large withdrawal svb had to sell some of their long term bonds to cover the transaction.

For some time the bank had enough liquidity to deal with these withdrawals as time passed the depositors continued to leave. On March 8th 2023 svb made a bombshell announcement; there was selling off their entire liquid bond portfolio worth over $21 billion until this point the falling bond prices were only unrealized losses, that is losses only on paper but once sold svb took a $1.8 billion dollar loss in the sale. To recoup some losses management decided to raise some capital while this seems like a logical choice, this was a grave error from management the timing could not have been worse.

Just days before silvergate a small crypto focus bank failed due to a similar issue although this failure had more to do with the exposure to the overall crypto market and FTX in particular but the root cause was the same the bank had a lot of assets which had lost their value due to rising interest rates and when withdraws in the crypto market began to happen they had no choice but to sell those assets each sale of the assets was a lower price than when they bought it. Once the losses piled up there was no turning back, investors assumed that svb was going down the same path. Fears over insolvency issues quickly spread and this resulted in svb stock losing close to 60% percent of its value in one day.

As all of this unfolded many venture capital firms advised the founders of startups to pull their money out of SVB further exacerbating the problem. By the end of March 9th customers had withdrawn $42 billion dollars leaving the bank with a negative cash balance of about -$958 million. The withdrawal was so heavy that it ended up crashing the banks and tunnel system, only creating more fear. Depositors had a reason to panic, in the United states under the Federal deposit insurance corporation or FDIC the US government only guarantees refunds up to $250,000. Now the thing is being a technology company focused bank 97% of svb deposit exceeded this number.

The silicon valley bank shares continued to be destroyed until its trading was suspended on the morning of march 10th. They tried to raise capital and failed and then by midday on march 10th the bank started to look for a company to bail them out and no one wanted to touch them. Nobody knew the extent of the problem so it was a risk, this culminated in being shut down by the FDIC.

This all happened on March 10th less than two days after the crisis started. This was a spectacular failure on the side of management; they failed to adjust to the rising interest rate environment. And yes the US federal reserve got it wrong when they stated that inflation was only transitory. But SVB should have had a contingency plan just in case inflation did stick around.

If any of you reading works in risk management especially in banking I would love to hear from you in the comments below on what a contingency plan could have been.

It seems that as soon as interest rate started rising the bank could have began to offload the long term treasury’s and exchange them for bonds yielding high interest to minimize their losses. Instead it seems that they waited and sold all of their liquid long term bonds at once after the value had already fallen.

As Bill Ackman (Founder, CEO, Pershing Square Capital Management, L.P.) states “Silicon valley bank senior management made a basic mistake: they invested short-term deposits in longer term fixed-rate assets”. So how could management do such a thing? The story gets a bit wilder the more that you look.

As people began to dig deeper into this crash some new information painted a very worrisome picture. The chief risk officer for silicon valley bank high tailed and left in april of 2022 and wasn’t replaced until january of 2023. This meant that the bank had no chief risk officer for eight months. This was precisely at the time when the downward feedback loop was accelerating from the high interest rates.

Just when the bank’s portfolios needed to be rebalanced to account for high interest rates there was no one to oversee the process, in other words the bank was a plane without a pilot during a storm. Just shocking!. But it doesn’t end there worse yet silicon valley bank CAO (Joseph Gentile) was the CFO of none other than Lehman Brothers at the time of it’s crash.

And I can’t help but laugh at how ridiculous this next part is. The federal reserve bank of san francisco was in charge of supervising svb and guess he was on the board the CEO of svb Greg Becker.

Greg was probably eaten from the board after the crash. Interestingly the CEO, CFO and CMO of the bank sold a combined $4.4 million dollars of company stock just weeks before svb declined.

An SCC filing stated that the sale of the shares was “automated” and “pre planned”, but it remains unclear if there was some knowledge of the collapse. Further to this the bank’s employees received their annual bonuses ranging from $12,000 to $140,000 only hours before the bank’s official crash.

I can’t allege implications of wrongdoing but there may be a chance that the guys at the top knew something was coming.

Right now SVB is being sued for fraud by shareholders the lawsuit states: The company failed to disclose how rising interest rates could leave the bank particularly susceptible to a bank run.

A crash of svb wasn’t indeed unique a combination of rapid growth bad risk management low interest rates excessive exposure to only one market and large deposits with no FDIC insurance have all led us to this point.

But is this the start of something bigger for the financial system is it a lehman moment.

It may very well have been a lehman moment for regional banks as they have similar characteristics to svb their clients or businesses they operate in a very limited number of films and they all have some exposure to unrealized losses in this higher interest rate environment.

Because of this the stocks of first bank republic, western alliance bancorp and westpac bancorp and other regional banks have all seen large declines, some as much as 66% in a day. many hedge funds have also started to short

The falls of the stock prices was so drastic that the trading of a slew of these banks had to be halted

Okay so this next part is key

Right at this moment the rest of the banking system seems to be largely unaffected as one analyst at Barclays wrote “ deposit pressure is the greatest for smaller banks including regionals. [Global banks] have more diverse funding sources and therefore are less vulnerable to that risk.”

That being said bank of america does have large exposure to long term bonds that are planned to be held to maturity though if they don’t so and actually hold these points to maturity this shouldn’t be a problem.

Many are comparing the situation to that of the 2008 financial crisis yet this is quite different. During that time some of the largest banks in the US all felt simultaneously and they had much bigger issues to do with these banks having sizable investments and assets that overnight became worthless.

The assets that are responsible for the crash of SVB are not worthless in fact far from it they backed by the us government and if held felt maturity in theory the not going to lose any value.

The problem for SVB is that they sold all of these bonds early and realize those losses tried to raise funds to cover those losses and that triggered a panic

Another difference resides in the fact that the banks in 2008 had huge leverage issues. in the case of lehman brothers for example the leverage exceeded 30 times the underlying asset in other words a decline of three to five percent in those assets meant that lehman brothers was completely bankrupt and lastly the big banks have a far greater degree of diversification than regional banks this means that they can withstand liquidity shocks more easily as generally not every single sector gets impact of the same time.

Not only this but the big banks will probably benefit from the collapse of regional bank depositors may move the money from regional banks to large institutions and if there are more bank failures for larger banks can simply gobble up the healthy parts for pennies on the dollar.

Does this mean that the risk of a financial crisis is nonexistent or not really. while the current financial system is very different from the one in 2008 there is still a chance that this may be the first crack in the fabrics of the current financial system

As of december 2022 the total unrealized losses for the whole banking system was close to $620 billion

If panic spreads too much many small banks will go down as a result creating a cascading effect that would cause the rest of the economy to wobble. the federal reserve and the financial sectors of the us government have recognized this and have come up with a solution which will get to shortly.

The industry that will feel the most pain is going to be the tech sector.

“SVB was the lifeblood of the tech ecosystem” states Ro Khanna a congressman from california 17th district tens of thousands of startups rely on them to pay for their day to day operations including stuff. you see unlike traditional businesses many of these tech companies have negative cashflows the only way that they can pay their expenses is by raising capital.

After the capital has been obtained they store it and use it until the next raise if you take that stored money away very quickly many of these from start to fail.

Several firms aren’t going to be able to pay their employees and if this further delays and when the money is returned a huge wave of layoffs and then eventually bankruptcies will follow.

Etsy had to delay their silipads, the streaming company ROKU held a quarter of its cash reserves in SVB. ROBLOX, Rocketlab, Circle, VOX Media and vimeo are among countless companies affected the CEO of Y Combinator Garry Tan puts it best “this is an extinction level event for startups and will set back the innovation by ten years or more”

Confidence in the finance industry has been shaken US banks lost a combined $100 billion and $50 billion for the valuation of european banks.

On the 13th of Match Joe Biden had to reassure the united states population.

The situation also spread to the UK.

The Bank of England was looking for ways to minimize the damage. The united kingdom also had an arm of silicon valley bank then on march 13th hsbc bought the stricken SVB UK entity for measly 1 pound or 1.25 us dollars. At the height of the chaos two hundred uk firms confirmed that they weren’t going to be able to pay their staff. On the other side of the world chinese startups also reported issues accessing the funds svb was especially popular among chinese biotech startups. as one founder explained “we tried everything on friday morning but it was already too late. The transfer is still processing.

It’s very crazy we; didn’t think this could happen”

For Chinese groups the ecosystem was already damaged by Beijing’s tech crackdown and Covid19 pandemic controls, not to mention the rising geopolitical tensions with US, India and other countries.

So in all of this where were the regulators. well being lobbied apparently. Back in 2015 SVB CEO begged lawmakers to exempt banks with assets less than $250 billion from the tough supervision and regulations of the Dodd–Frank Act. This act was put into place to stop another financial crisis.

In 2018 a bill was passed that weakened this act and Greg Becker got his wish. Saule Omarova a professor of law at Cornell University, testified before the senate against relaxing regulations for smaller banks said that the 2018 bill “should not have been passed” and he was spot on.

The chaos has subsided a bit. Upon taking over control of Silicon Valley Bank, the FDIC transferred SVB deposits to a newly created holding account and appointed Tim Mayopoulos as CEO.

Another regional bank, Signature Bank, failed in March 2023.

As other potential bank collapses loomed, the Federal Reserve was forced to take extraordinary action and announced the establishment of a bank term funding programme to support liquidity for other banks that were at danger.

They are enabling the impacted banks to sell the long-term bonds and securities to the Fed without suffering a loss. The treasury, federal reserve, and FDIC declared that all depositors, even those who are not insured, will be paid whole without using taxpayer funds in a separate announcement made on the same day.

This is an inflationary move, according to some financial pundits.

There are many regional banks that operate similarly to SVB, causing anxious depositors to gather outside to withdraw their money. To prevent bank runs and a string of bankruptcies, the Fed and the US government were forced to take these severe measures.

Nobody’s a fan of government assisted bailout but this is a tough situation. As Simon Johnson and economist at mit he previously served as the chief economist of the IMF says “All choices are bad choices, you don’t want to extend this kind of bailout to people. But if you aren’t doing that, you face a run of really big – and really hard to predict – proportions.”

Since the financial crisis, this has been the biggest banking failure. The effects on businesses all around the United States could be disastrous if the federal government’s implementation of the bank term funding scheme isn’t as seamless as promised or takes too long.

Despite my opinion that the federal reserve is partially to blame for the general macroeconomic predicament, action was required. In addition, inflation could increase once more, wreaking much more misery, if the Federal Reserve starts decreasing interest rates for good reason. They are caught between two cliffs: raising rates will destroy the economy, and cutting rates will do the same.

65000 startups will be impacted by the collapse, with silicon valley accounting for 50% of US VC-backed startups’ clients. Even if the government is successful in making all the deposits, this is a sad time for the tech industry since confidence has been lost. There will be a scar from the terror of being shut out due to company cash flow troubles, personnel payments, and many administrative problems.

In conclusion, this is a tale of risk management failure, lobbying, and quickly shifting market conditions.